At its 2026 Upfront, Amazon stopped acting like a retail media network and started acting like a TV network with a checkout button. Most health and nutrition brands haven’t restructured their playbooks. Here’s what that costs them.

Let’s be honest. Most health and nutrition marketers I talk to still treat Amazon as a conversion line item. It sits in the retail media budget. It reports up through e-commerce. It gets measured on ROAS. And it never crosses paths with the brand team running CTV, the social team running awareness, or the CRM team thinking about loyalty.

That model is broken. And on May 11, 2026, Amazon made it official.

At its 2026 Upfront at the Beacon Theatre in New York, Amazon Ads put a single message in front of every agency buyer in the room: this is no longer a retail media platform. It’s a full-funnel commerce media ecosystem that spans streaming TV, live sports, Twitch, podcasts, creator content, Amazon DSP, and Amazon Marketing Cloud. All connected. All measurable. All sitting on the same authenticated identity graph.

If you work in health, beauty, nutrition, or any category where consumer trust matters more than impressions, what Amazon just announced changes how your media plan should look in 2027. Here’s what actually shifted, what the data says, and where I’d put my budget if I were rebuilding the plan from scratch.

What Amazon Actually Announced

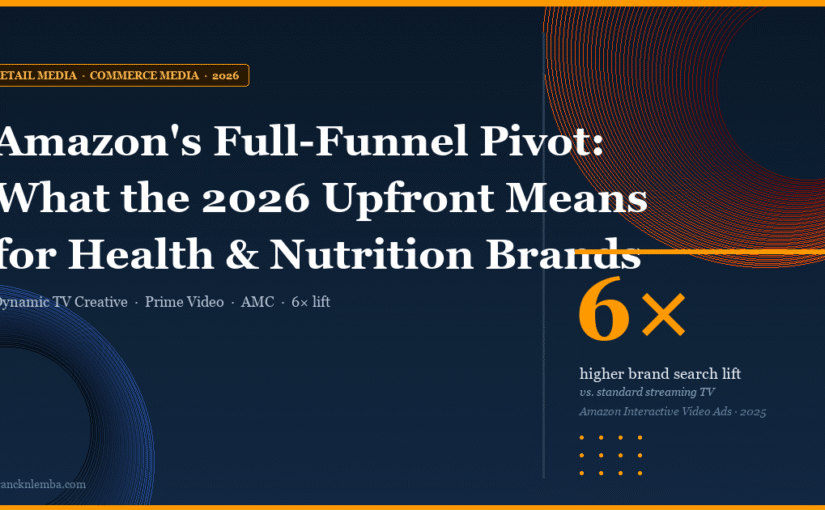

The headline from the 2026 Upfront was a new product called Dynamic TV Creative. It’s the first capability inside Amazon’s Prime Video ad stack that automatically personalizes Interactive Video Ads based on a viewer’s shopping behavior and where they sit in the purchase funnel. Same ad asset. Different version. Adjusted at the moment of impression.

The way it works is straightforward. A viewer who has never seen the brand gets a standard awareness-style ad with a “learn more” call-to-action. A viewer whose shopping signals suggest purchase intent gets a different version with pricing, ratings, and an “add to cart” button. The product imagery, headline copy, and on-screen details all shift based on what Amazon’s authenticated graph knows about the viewer. It launched ahead of the Upfront for select U.S. advertisers in CPG, fashion, and electronics, with wider rollout planned for Q3 2026, including live sports.

That’s the new product. But the bigger story is the system around it.

Source: Amazon Internal, Interactive Video Ads Incrementality Study 2025

Those numbers are the part that should make any digital director uncomfortable. They’re not benchmark lifts against a poorly run campaign. They’re lifts measured against standard streaming TV. The implication is clear: if you’re still buying CTV the old way, you’re leaving outcomes on the table that a competitor running the new format is collecting.

The authenticated graph at the center of everything

The product announcement matters. But what makes it work is Amazon’s authenticated graph, which the company says reaches 90% of U.S. households. Not modeled. Not panel-based. Authenticated through Amazon sign-ins, Fire TV registrations, Prime Video streaming, shopping behavior, and entertainment touchpoints.

Why does that matter for a health and nutrition brand? Two reasons.

First, frequency management actually works. In traditional CTV planning, you assume a household, you assume a demo, and you hope the frequency curve looks something like what you bought. With deterministic identity, you know who you reached, how many times, and what they did next. That’s a different kind of media plan.

Second, and this is the part I keep coming back to, the same graph that powers ad delivery also powers measurement inside Amazon Marketing Cloud. The exposure data, the shopping data, the conversion data, the repeat purchase data, the Subscribe & Save data. All in one clean room. For a category that gets evaluated on lifetime value and repeat behavior more than on a single conversion, that’s not a media improvement. That’s a customer engagement infrastructure upgrade.

Why This Matters More for Health and Nutrition Than for Snacks

Here’s where I think most analysis of the 2026 Upfront gets too generic. Amazon’s pitch applies to every category, but the value isn’t equal. For categories driven by impulse and shelf placement, the upper-funnel investment is a nice-to-have. For categories driven by consumer trust, education, and repeat purchase, the upper-funnel investment is the whole game.

And the data backs that up. eMarketer’s April 2026 industry KPI report shows retail media spend growth in health and beauty jumped more than 50% year-over-year, well ahead of every other category. That’s not happening because the category needs more retail ads. It’s happening because the brands inside the category figured out that retail media is where they can finally pair brand-building with measurable purchase outcomes.

What I tell my team is that in our category, three things are non-negotiable: trust, context, and proof. Amazon’s authenticated reach handles context. The measurement stack handles proof. Trust is something the brand has to earn through the content adjacency it chooses and the creative it puts out. The platform doesn’t do that part for you, but it gives you environments where it can actually happen. Trusted podcasts. Premium sports. Curated streaming. None of that existed inside the old retail media bucket.

“In our category, three things are non-negotiable: trust, context, and proof. Retail media used to handle one of them. Amazon’s full-funnel stack now handles all three.”

A Story from a Real Brand: Aveeno Baby

An emerging brand with no website. Nine weeks. Six million parents reached.

Aveeno Baby had a problem that should sound familiar to a lot of health and personal care brands trying to crack a new market. In India, the brand was still emerging. There was no owned e-commerce site. Sales lived inside Amazon. And the audience they cared about, parents of newborns to three-year-olds, was scattered across streaming services, social platforms, and third-party apps.

The team at Interactive Avenues didn’t run a search-only campaign. They didn’t run a display-only campaign. They built a full-funnel plan on Amazon DSP. A 15-second in-stream video to drive awareness. Static creatives and responsive digital ads across third-party apps to push consideration. All of it directed back to the best-selling Aveeno Baby product detail pages on Amazon.

Nine weeks later, the campaign had reached six million parents. Branded searches climbed 22%. The base of brand searchers and browsers grew sixfold. A Nielsen brand lift study measured an 11% increase in brand awareness among exposed audiences. And the total customer base for Aveeno Baby grew 18%.

The part I find most useful for our category isn’t the lift numbers. It’s the architecture. The shoppers who saw both ad formats, video and display, experienced an 8x increase in purchase rates compared to those exposed to a single format. That’s not a creative optimization. That’s a media architecture decision. Run one format and you get a fraction of the outcome. Run them together inside the same identity graph and the math changes completely.

The Second Story: H&R Block and Privacy-Safe Full-Funnel

A brand that doesn’t even sell on Amazon, doubling conversion through Amazon Ads.

I include this one specifically because the parallel to health and nutrition is closer than it looks. H&R Block doesn’t sell most of its products on Amazon. Neither do a lot of health brands that face channel complexity, compliance constraints, or partnership structures that limit what they can do on retailer platforms.

What H&R Block did was use Amazon Ads as a media and audience layer, not just a retail platform. They used Brand+ for AI-powered awareness across streaming TV and online video, including Prime Video. They used Performance+ for lower-funnel display and OLV. They built custom audiences inside Amazon Marketing Cloud and used hashed first-party data to keep everything privacy-safe.

The results from the 2025 tax season tell the story. Online video CPMs improved 26% year-over-year. Cost per acquisition improved 35%. Adding OLV to display alone drove a 47% lift in conversion rates. Adding Prime Video on top pushed that lift to 66%. And the full-funnel strategy more than doubled conversion rates compared to display-only campaigns, delivering a 144% total increase. Custom AMC audiences also delivered 62% more efficient CPA against the brand’s display average.

What’s the lesson for a regulated, compliance-heavy category like health and nutrition? You don’t need to live entirely inside Amazon to use Amazon as a full-funnel engine. The graph, the inventory, the measurement, and the audience-building tools are usable whether or not your primary checkout sits on the retailer’s platform. That’s a meaningful shift, and it opens the playbook for a lot of brands that have been told they don’t have an Amazon strategy because they don’t drive Amazon sales.

The Canadian Context (And Why It’s Already Different)

I write about the Canadian market a lot, so let me bring this home. The Amazon Upfront is a U.S. event. The product launches are U.S.-first. But the shift it signals is more advanced in Canada than most marketers realize.

According to eMarketer’s analysis, Canada ranks second in the world, behind only China, in retail media’s share of total digital ad spend. And the reason is Amazon. Amazon.ca’s dominance in Canadian e-commerce gives Amazon Ads a structurally larger share of the Canadian retail media market than it has in most other countries. Retail media spending in Canada will reach C$3.8 billion in 2026, and digital will account for 80.1% of total media ad spend.

What this means in practical terms is that a Canadian marketer who treats Amazon as a sponsored search bucket is mis-allocating against the realities of their own market. The full-funnel argument isn’t a future-state pitch in Canada. It’s already where the budget is moving.

Try It Yourself: The Full-Funnel Lift Calculator

What does a full-funnel approach actually do to your numbers?

Drag the sliders to model an Amazon DSP investment and see how a single-format plan compares to a full-funnel plan. The lift assumptions are based on the real H&R Block (144%) and Aveeno Baby (8x) case studies and the Interactive Video Ads incrementality study (5x purchase rate).

6.25M

312

762

$14,063

$34,313

+$20,250

Illustrative model only. Real outcomes depend on category, creative quality, audience strategy, PDP readiness, and measurement methodology. Lift multipliers sourced from Amazon Ads case studies cited at the bottom of this article.

The Three Mistakes I See Most Often

1. Reporting Amazon on ROAS alone

If your Amazon scorecard ends at ROAS, your media plan is going to keep collapsing toward the bottom of the funnel. ROAS rewards harvesting demand. It does not reward creating demand. And in a category where the next purchase, the third purchase, and the Subscribe & Save renewal matter more than the first one, optimizing for ROAS will quietly starve your future growth. The H&R Block case study didn’t get published because of ROAS. It got published because the team measured cost per acquisition, conversion lift, frequency reduction, and AMC audience efficiency. That’s the scorecard.

2. Separating brand and retail budgets

This is the structural problem I see in almost every organization. The brand team owns Prime Video. The retail team owns Sponsored Products. The two budgets are planned separately, measured separately, and rarely talk to each other. Amazon’s pitch is that the funnel is one system. If you keep planning it as two systems, you don’t get the lift the platform is capable of delivering. According to Marketing Dive, the full-funnel campaigns offering launching this year is designed to unify sponsored ads, display, and streaming TV in a single agentic AI tool. That tells you where Amazon thinks the work should sit.

3. Scaling media before PDPs are ready

This one is the unsexy truth that nobody wants to put on a slide. Amazon media will not save a weak product detail page. If your images are mediocre, your copy is unclear, your reviews are thin, your claims are not properly substantiated, or your comparison story is confusing, scaling Prime Video spend on top of that will just deliver more shoppers to a page that doesn’t convert. I’ve seen this firsthand more times than I want to count. Fix the PDPs. Then scale the media.

What to Do Monday Morning

Five practical moves for the next 90 days

- Run one full-funnel pilot. Pick one brand and one priority audience. Build a stack with streaming TV awareness, Amazon DSP retargeting, Sponsored Brands capture, and AMC measurement on top. Don’t pilot everything. Pilot one thing properly.

- Rebuild the Amazon scorecard. Add reach, frequency, branded search lift, PDP views, first-time buyers, repeat purchase rate, and an LTV proxy. Keep ROAS as one metric among many, not the only one.

- Set up an AMC learning agenda. Exposed versus non-exposed shoppers. First-time buyers. Branded search lift. Subscribe & Save renewal. These are CRM questions, not media questions, and AMC is built to answer them.

- Audit your PDPs before you scale media. Images, claims, reviews, comparison content, subscription options. If the page isn’t ready, the media won’t carry it.

- Pick your content context deliberately. Sports for active-living audiences. Premium streaming for adult education plays. Twitch for younger occasion-based brands. Trusted podcasts for high-consideration health stories. Inventory choice signals brand positioning. Don’t outsource the decision to a media plan.

The Bottom Line

Amazon’s 2026 Upfront wasn’t really about a single product launch. Dynamic TV Creative is interesting. The 6x and 5x lift numbers are interesting. But the actual signal is structural. Amazon is telling the market it has assembled the full stack: deterministic identity, premium video inventory, sports, audio, creator content, programmatic, retail conversion, and clean-room measurement. All inside one system. And it is openly betting that the brands willing to plan against that system as one connected funnel will out-grow the ones that don’t.

The brands that win this next phase won’t be the ones that spend more on Amazon. They’ll be the ones that stop treating Amazon like a checkout aisle and start treating it like what it is becoming: the most complete commerce media network in North America, with a measurement layer that finally lets you connect a Prime Video impression to a Subscribe & Save renewal eighteen months later.

That’s the part most playbooks haven’t caught up to yet. The brands that close that gap first are the ones I’d bet on.

Sources & further reading

- Amazon Ads, Amazon Upfront 2026 recap: Series, movies, sports, ads news (May 2026)

- Amazon Ads, Aveeno Baby boosted brand awareness and conversion with a full-funnel strategy

- Amazon Ads, H&R Block drives full-funnel success (November 2025)

- AdExchanger, Amazon’s Interactive CTV Ad Suite Now Includes Creative Optimization (May 2026)

- Marketing Dive, Will Amazon’s AI-powered one-stop shop for advertising change the game? (November 2025)

- eMarketer, Canada Retail Media 2026 (January 2026)

- eMarketer, Retail media is the fastest-growing digital advertising channel at scale in Canada

- eMarketer, FAQ on retail media networks: How marketers should allocate budgets in 2026

- Wikipedia, Amazon Advertising

- Wikipedia, Amazon Marketing Cloud